P.S.: Petit cadeau pour tous ceux qui sont interesses par une collection de ses "papers" (fin annees '70 - fin annees '90) de Paolo K. ....(papers dont ceux des annees '70 - debut annees '90 sont tres interessants dans le "contexte geopolitique" d'antan...)

(cliquer sur le texte en haut pour en savoir +)

(cliquer sur le texte en haut pour en savoir +)

"Ideology, oh thou Ideology"...

where have you gone...and what have you done...?

(click on the pic to get directed)

(click on the pic to get directed)

Shocking! Simply shocking!...

(add. du 02.02.2008)

Sans doute, un facteur majeur (entre x-autres...) qui contribue aux "dynamiques du capitalisme"...

(veuillez cliquer sur l'image pour en savoir +...; click on the image above to get more informations...)

"Non vitae, sed scholae discimus" (plus ça change...)

(veuiller cliquer sur le texte au-dessus pour en savoir +...; click on the text above 2 get directed 2 the reference...)

Ah bon..?

"--especially, in this case, mortgage debt (endogenous) and partly the stock-market (s-m.: exognenous & endogneous)"

Bingo...!?

"Collective humility" (in german)...

Add. du 08.05.2009:

Humility vs. "strict-hierarchically-structured" Education (in italian)

(Franco Modigliani: Avventure di un economista, p.191-192)

En avant-première...

leaked "off-the-record" speech between B.O. and Krugman...

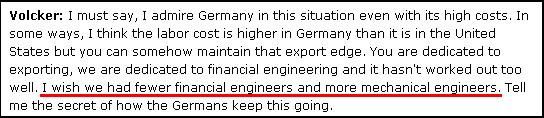

"F@&§*#g scary !" (part I)...

(click on the image above to get linked)

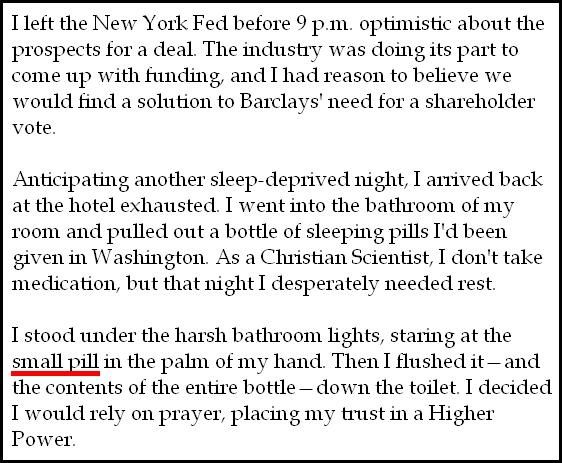

"F@&§*#g scary !" (part II)...

(click on the image above to get linked)

"This was nostalgia in the literal Greek sense: the pain of not being able to return to one's home and family."

ROTFL!!!

ROTFL2!!!

The too much "illusory/perfect" function...

No comment...

1.93bn €...("Il denaro non è l'idea, ma compera i padroni dell'idea.")

Obama needs to be bold on trade...

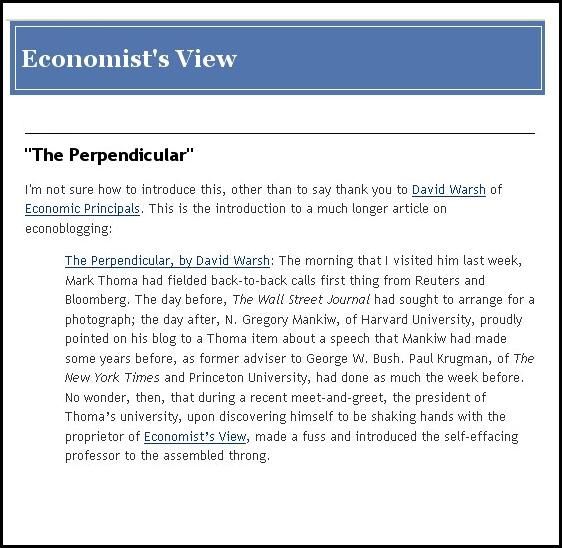

Civil Servant & Self-Effacing Mark Thoma is (absolutely rightly !) getting praised for his long-time work & efforts (Congrats on the well-deserved kudos !)

Argument...!

Via CR...

Fredmund F. M. im HB...

Pancho, speaking for himself...

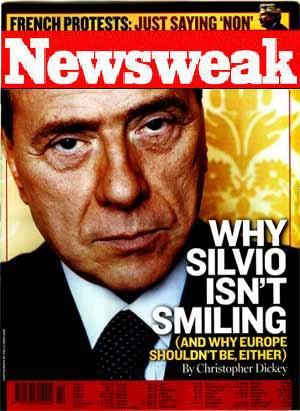

"Newsweak" & "Tame Magazine"...

To whom the smile...?

("...and the frozen cannot have"...= "Sesshaftigkeit"... vs. "Mobility"...-Edition)

Tito Boeri@Handelsblatt.com

Update 23/08/2009

"Blog-Alarm"....

(clic on the pic to get directed...)

(clic on the pic to get directed...)

(clic on the pic to get directed)

(clic on the pic to get directed)

two, iP'so, terribly interesting blogs either due to their "sarcastic/ironic/witty touch/tone"...or...to the "analytical depth" (at times, a justified "higgledy-piggledy" trip through the fields of economics, natural sciences, social sciences, history, maths, etc. etc. etc. to get to their point...) their editors are willing to share with the whole world outside...

In that sense, Pancho must really toll them respect for what "Nathan A. Martin & Hellasious" are doing....keep going on with this excellent job, guys...

P.S.:goddamit... why not have discovered these blogs earlier...

Hhhhmmm...!????

"Pancho" plaide..."Non coupable !"...

OUCH!

HUH! (Ned Phelps-Edition)

"Carry-Trading" vs. "Equities purchasing"...

"Au pif"... Σ (Volatility) as f (FOREX) -> +/- C., donc...

Hasta...

"PRISA", subiendo la la presión de "GS"...?

"Let me show you, Let me show you the way to go..."

(John Kay & Martin Wolf Edition)

{kind=link}